Listen to a podcast discussion about this article.

One of the enduring fantasies of modern life is that the people sitting atop oceans of oil pray for gasoline prices high enough to make a Pittsburgh commuter wobble beside the Sheetz pump in Center Township.

This is understandable. We assume that if something is valuable, its seller wants the highest possible price. The hot dog vendor hopes for hungry crowds. The umbrella seller prays for rain. So Americans imagine Saudi princes plotting under crystal chandeliers to turn a Beaver County family vacation into a federally subsidized bicycle ride.

But oil is not hot dogs. Oil is far stranger: a commodity so valuable that its owners fear making it too expensive.

That’s the central lesson of the global petroleum business. The oil kingdom’s greatest nightmare is not low prices. It is prices so high they finally persuade the world to stop needing oil.

This requires understanding the key distinction economists make between “production break-even” and “fiscal break-even.” Production break-even is simply the cost of pumping one more barrel out of the ground—expenses like labor, maintenance, and basic operations. Fiscal break-even is the much higher oil price a government needs to balance its national budget and pay for everything the state spends: roads, subsidies, salaries, military, palaces, social programs, and the cost of keeping the population content.

Saudi Arabia can pump oil from the giant Ghawar field for roughly three dollars a barrel—cheaper than a small popcorn at the Monaca Cinemark. Nature does most of the work. The reservoirs are massive, pressurized, and generous. That is their production break-even.

American fracking, by contrast, is more like keeping an aging Buick running on duct tape, borrowed money, and prayer. Fracking wells decline rapidly. They demand constant drilling and prices north of $60–$70 a barrel to make economic sense.

Yet while Saudi oil is physically cheap to produce, the Saudi state cannot survive on three-dollar oil. Their fiscal break-even is dramatically higher because the royal family funds an entire civilization with petroleum revenue.

That tension has quietly shaped modern world history.

At the 1976 OPEC meeting in Doha, eleven of thirteen oil-producing nations wanted sharp price hikes. Iran, under the Shah, needed them desperately. The Shah was on a historic spending spree: military buildup, infrastructure, modernization. Iran required roughly $19 oil to keep the dream alive.

Saudi Oil Minister Ahmed Zaki Yamani walked out, consulted the royal court, and returned with a firm no. The Saudis accepted only a modest increase and threatened to flood the market with an extra three million barrels a day if necessary.

To outsiders, this looked insane. Why refuse easy money?

Because the Saudis understood a fundamental truth about commodities: prices that rise too high invite substitutes.

The classic precedent is rubber. When Britain controlled most natural rubber through Malaysian plantations and drove prices skyward, Germany and the United States faced a national security crisis. Massive investment poured into synthetic rubber. Within decades, Britain’s monopoly was broken.

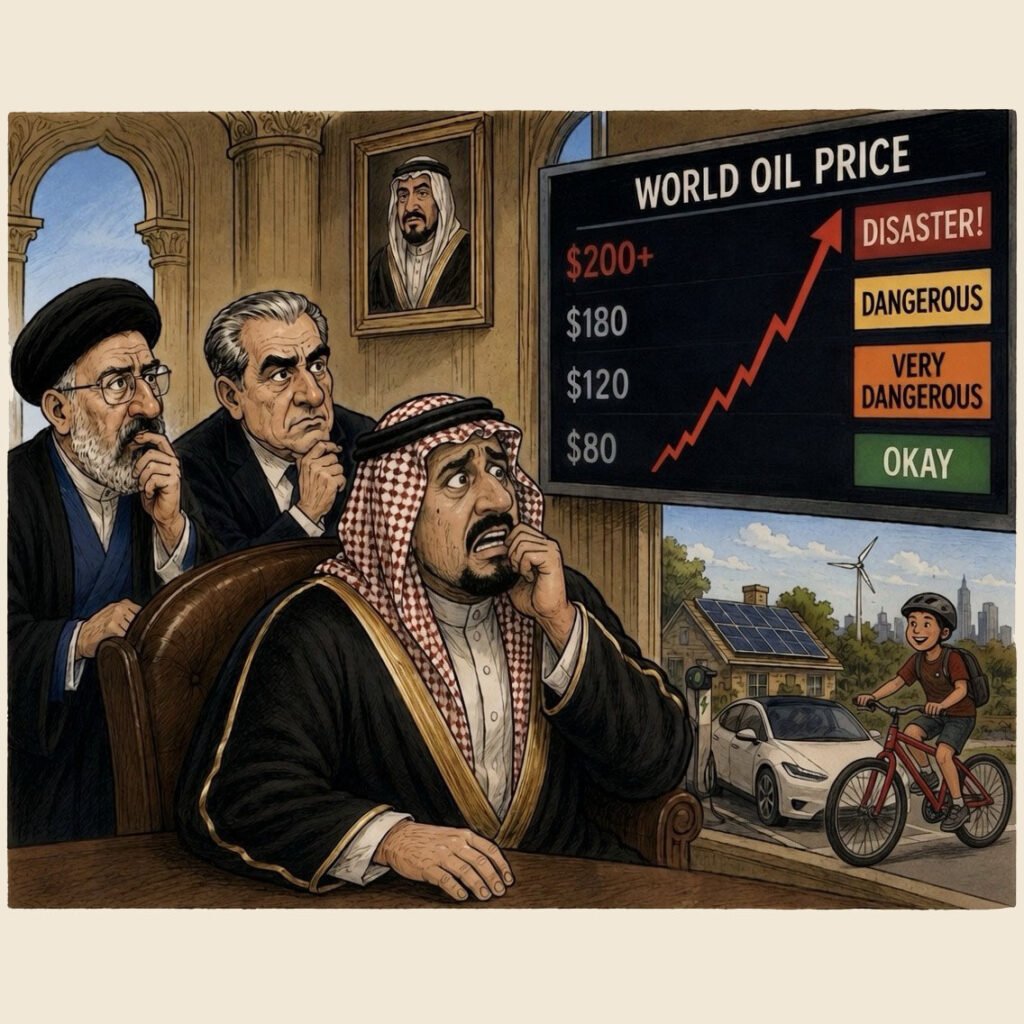

Oil producers fear the same outcome. If crude rockets toward $200 a barrel, complaints about electric vehicles and nuclear power turn into enthusiastic adoption. Engineers suddenly become miracle workers. Nuclear becomes politically palatable. Solar panels appear everywhere.

High oil prices do not maximize long-term profits. They accelerate the arrival of a post-oil world.

Yamani captured this wisdom perfectly: “The Stone Age didn’t end because we ran out of stones, and the age of oil won’t end because we run out of oil.”

Saudi strategy therefore aims to keep prices high enough to meet their fiscal break-even and fund the state, but low enough to discourage panic-driven innovation.

This explains why the Saudis sometimes act like a farmer burning his own cornfield. In 2016, rather than cutting production to support prices, they allowed oil to collapse in order to crush heavily indebted American fracking companies. Bankruptcies swept through the U.S. shale patch. It was ruthless, painful—and, from Riyadh’s perspective, entirely rational. Better to protect market share today than lose customers permanently tomorrow.

There is a lesson here for Western Pennsylvania, where the ghosts of past industrial booms still linger.

Energy transitions rarely occur because of sudden moral awakenings. They happen when economics shifts beneath people’s feet.

Ironically, the 1970s oil shocks briefly made nuclear power look attractive. But the inflation those shocks helped create drove interest rates to punishing levels, making the huge upfront costs of nuclear plants nearly impossible to finance. America partly strangled its own nuclear future with the very economic chaos caused by energy panic.

History often works like a man fixing a furnace with a hammer—every fix creates three new problems.

So the next time oil prices spike and pundits predict either the end of capitalism or the dawn of utopia, remember: somewhere in Riyadh sits a very nervous man in a very expensive robe, hoping prices do not rise too much.

Because in the oil business, what goes up eventually gives somebody a very strong reason to bring it back down.